Anne Heche Died in 2022. Her Family Is Still Paying for It

After you're gone, your family won't just be grieving. They'll be making phone calls, hunting down accounts, and navigating a legal process that no one told them about.

That's the part that can quietly drag on for years, whether an estate is large or relatively modest. And a story that's been playing out in the courts since 2022 shows exactly what that looks like up close.

When actress Anne Heche died following a car accident in August 2022, she left behind an estate with about $110,000 in assets and more than $6 million in creditor claims, incomplete financial records, and a son in his early twenties who suddenly found himself appointed by a court to sort it all out. As of early 2026, that estate is still not closed. Nearly four years later, the family is still in the middle of it.

This is one example of what can happen when someone dies without a clear, updated plan and organized records. And the good news is, it doesn't have to happen to your family. Here's what this story reveals about poor recordkeeping, the burden placed on young adults, what significant creditor claims can do to an estate, and why the right planning makes all the difference.

Is Your Financial Life a Mystery, Even to You?

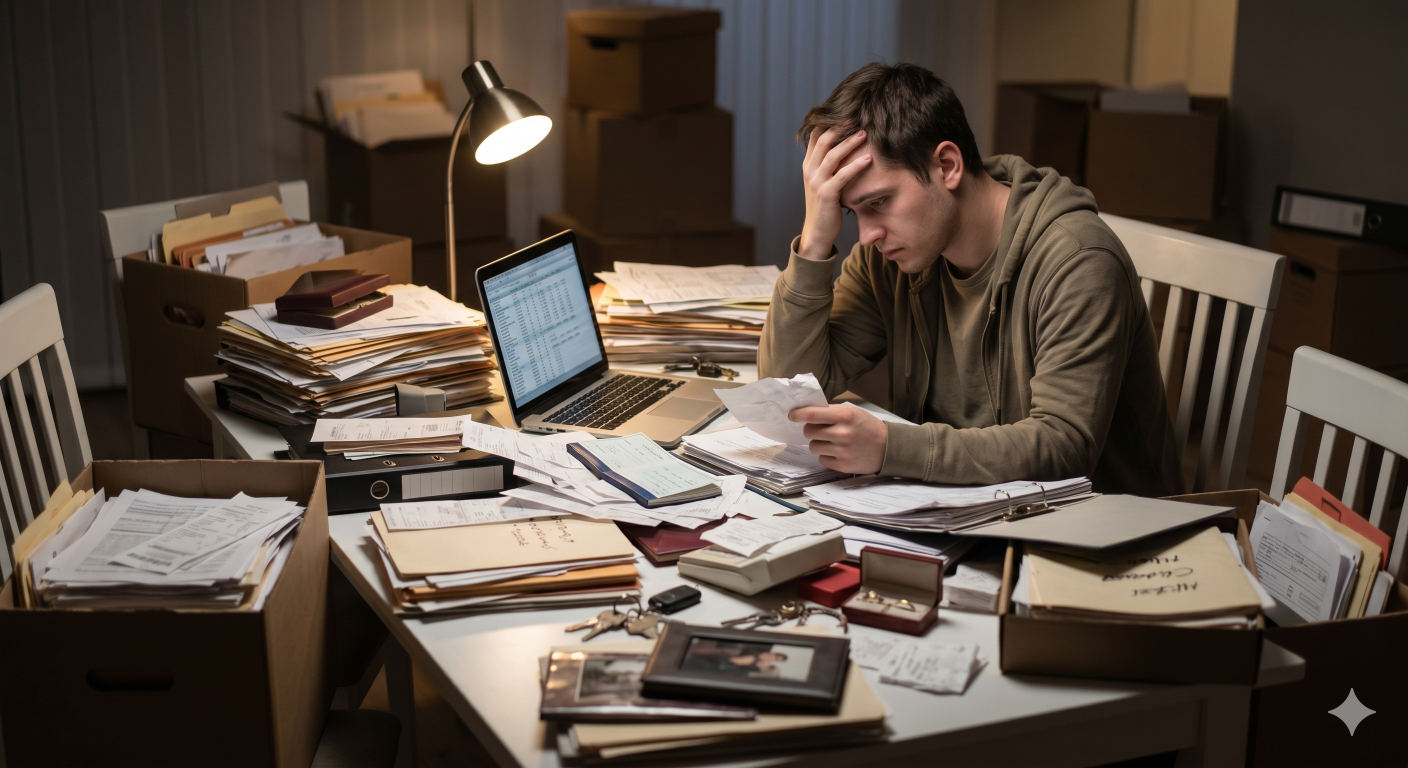

One of the most striking details in the Heche story is this: her son Homer couldn't account for all of her assets and income because, according to court filings, the records were disorganized and incomplete.

She had multiple income streams, including film earnings, a production company, a podcast, and various personal properties. But the recordkeeping was so poor that even tracking down what she owned took significant time and legal resources.

This is more common than most people realize. A lot of people have a general sense of what they own, but they haven't documented it in a way that anyone else could actually follow. When you're gone, your family isn't just grieving. They're also trying to figure out where your accounts are, what subscriptions are still being charged to your card, whether there are debts nobody knew about, and who actually holds the title to that property.

The bottom line: If your financial life were a mystery to your family right now, that's a problem your estate plan needs to solve before you die, not after.

A thorough estate plan starts with getting your financial life organized: creating a complete inventory of your assets, accounts, and obligations so your family isn't left hunting for answers at the worst possible time. It also establishes clear instructions for who handles what and in what order.

That foundation of clarity is what makes everything else possible. And it leads directly to the next question: once your family knows what you have, who are you actually asking to manage it?

The Person You'll Leave in Charge May Not Be Ready for This

Homer Heche Laffoon was in his early twenties when he was appointed administrator of his mother's estate. He was not only a grieving son. He was also barely and adult and suddenly responsible for untangling years of complex legal and financial issues while simultaneously dealing with lawsuits from multiple parties demanding millions of dollars.

It took him over a year just to prepare his first status report for the court. His attorney cited the sheer complexity of the circumstances as the reason things were moving so slowly.

Here's what that situation actually required of him:

Reviewing multiple active lawsuits and understanding the legal exposure

Tracking down incomplete records to identify and value assets

Negotiating with creditors over contested claims

Filing legal documents with the court on an ongoing basis

Making decisions that could affect the outcome of millions of dollars in claims

That's an enormous burden to place on anyone, let alone a young adult who is also processing the sudden loss of a parent.

The bottom line: Naming someone as your executor or administrator doesn't automatically give them the tools, guidance, or support they need to actually do the job. In addition, just because someone is part of your immediate family doesn’t mean they are the right person for the job.

A well-designed estate plan doesn't just name the right person. It sets them up for success. It provides clear documentation, pre-identifies advisors, and in many cases establishes a trust structure that simplifies administration and removes the need for court involvement altogether. When you plan ahead, you're not just protecting your assets. You're protecting the people you love from an impossible situation.

Of course, even the most prepared executor faces a harder road when creditors are involved. And that's where the Heche story gets even more instructive.

When Creditors Are Involved, the Stakes Change

The numbers in the Heche estate tell a striking story. Total assets: approximately $110,000. Total creditor claims: more than $6 million.

The largest claims came from the occupants and owners of the home damaged in the crash, who collectively sought around $6 million in damages. Her former partner alleged he was owed $157,000 in unpaid loans. There was also more than $36,000 in credit card debt.

Most families will never face claims of this size. But the underlying issue is not unique to celebrities.

An estate can face claims from medical bills, personal loans, credit cards, taxes, business obligations, or lawsuits. When valid claims are significant, they can reduce what ultimately passes to beneficiaries. In some cases, if claims exceed the value of the probate estate, heirs may receive little or nothing from that estate.

That does not mean every debt wipes out an inheritance, and it does not mean every asset is treated the same way. Insurance, exemptions, the type of debt, how an asset is titled, and state law can all matter. But the larger point is still worth paying attention to: debts and claims do not disappear just because someone dies.

That’s why estate planning isn’t just about who gets what. It is also about understanding what could put those assets at risk and planning accordingly.

Probate Avoidance and Creditor Protection Are Not the Same Thing

This is where a lot of online information gets fuzzy.

People often hear that a trust will “protect everything” or that avoiding probate keeps assets away from creditors. That is too simplistic, and in many cases it is not accurate.

For Missouri and Illinois families, a revocable living trust is often a very useful tool. It can help with incapacity planning, continuity, privacy, and probate avoidance. But it is generally not a shield against the trustmaker’s own creditors during life. Likewise, assets that pass by beneficiary designation may avoid probate, but that does not automatically make them untouchable in every circumstance.

Real creditor planning, when it is needed, usually requires a more careful analysis. That may involve looking at:

how assets are owned and titled

available insurance coverage

exempt versus nonexempt assets

business entity structure

beneficiary designations

whether irrevocable trust planning is appropriate

when and why transfers are being made

Timing matters too. Planning done well in advance is very different from trying to move assets after a claim has arisen or a lawsuit is already on the horizon. Once trouble is foreseeable, transfers may be ineffective or vulnerable under fraudulent transfer law.

The practical takeaway is this: good estate planning can often simplify administration and help certain assets pass more efficiently, but it should not be marketed as a magic barrier against all creditor claims. If creditor exposure is a real concern, that issue deserves its own strategy.

The Hidden Cost Nobody Talks About

The Heche estate has been in process for nearly four years. Legal fees, court costs, and ongoing negotiations have consumed resources that might otherwise have gone to her family. Her son has had to invest enormous amounts of time and energy into managing a process that, with clearer planning and better records, could have been far simpler.

Time is the hidden cost that most people don't account for when they think about what happens without a plan. It's not just money. It's months and years of your family's life spent navigating a system they never expected to face.

Even a modest estate, one without celebrity-level complexity, can take years to close if the paperwork is incomplete, the assets are hard to locate, or creditors are involved. And every month that process drags on, the people you love are still in limbo.

The bottom line: The time and money your family spends cleaning up an unplanned estate is often the most preventable cost in all of estate planning.

Why This Isn't a DIY Situation

There's no shortage of online tools that promise to help you create a will or trust for a few hundred dollars. And for some very simple situations, those tools might produce a document that looks legitimate on paper. But a document and a plan are not the same thing.

The Heche estate had assets. It had income streams. It had property. What it apparently didn't have was a coordinated, documented, professionally managed plan. That gap between having things and having a plan is exactly where estates fall apart. An attorney who takes the time to understand your full financial picture, your creditor exposure, how your assets are titled, and who you're really asking to step up can make sure your family isn't left piecing it together alone.

The bottom line: The goal isn't just to have documents. The goal is to have a plan that actually works.

What You Can Do Right Now

Nobody plans to leave their family with years of court proceedings and creditor negotiations. But without a thoughtful plan in place, that's exactly what can happen.

At Schroer Legacy Law LLC, we guide families through a planning process designed to bring order to the legal documents and the real-life details behind them, so loved ones are not left trying to figure everything out alone.

Schedule a complimentary 15-minute discovery call to find out where you stand:

This article is a service of Schroer Legacy Law LLC. We don’t just draft documents; we support you to make informed and empowered decisions about life and death, for yourself and the people you love. This material was created for educational and informational purposes only and is not intended as legal advice or services. Receipt or review of this article does not create an attorney-client relationship with Schroer Legacy Law LLC. If you seek legal advice specific to your needs, such advice and services must be obtained on your own, separate from this educational material.

The choice of a lawyer is an important decision and should not be based solely upon advertisements.